This glossary contains the words people can need in Accounting and Management

Accounts receivable

Noun

The amount of money owed by customers or clients to a business after goods or services have been delivered and/or used.

fr: Comptes débiteurs

Accrued Expense

noun

An expense that been incurred but hasn’t been paid is described by the term Accrued Expense.

Example: But why should you record accrued expenses before making the necessary payments? As a responsible business owner, you want your expenses to closely align with your revenues to increase accuracy in your firm’s financial statements.

fr: Charge à payer

Asset class

Noun

An asset class is a group of securities that behaves similarly in the marketplace. The three main asset classes are equities or stocks, fixed income or bonds, and cash equivalents or money market instruments.

Example: There’s some argument about exactly how many different classes of assets there are.

fr: Classe d'actifs

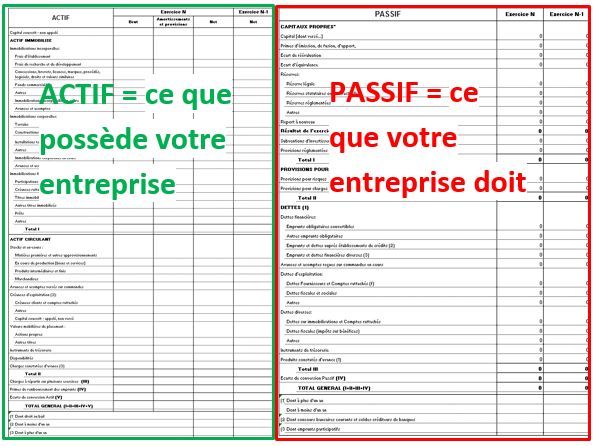

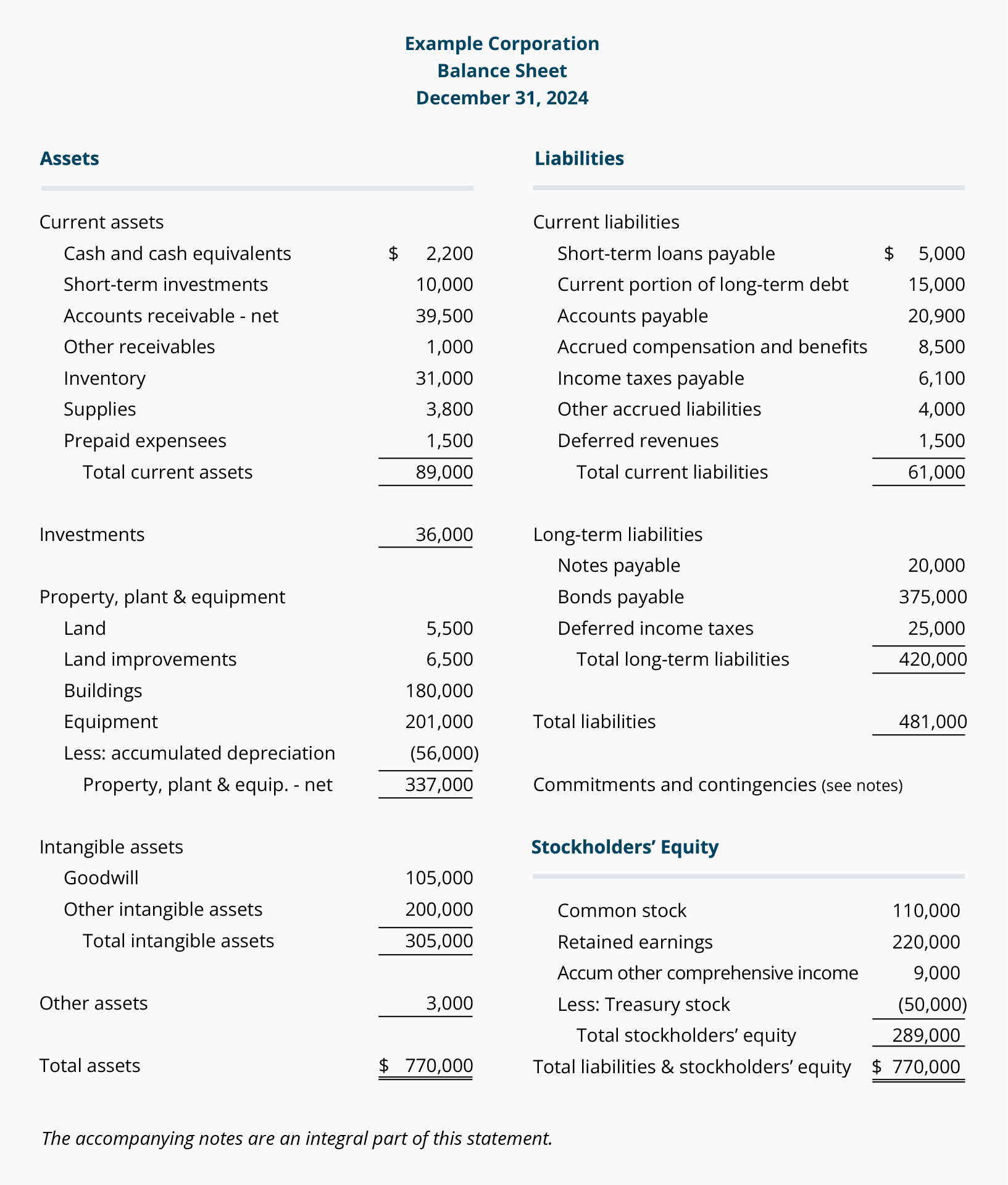

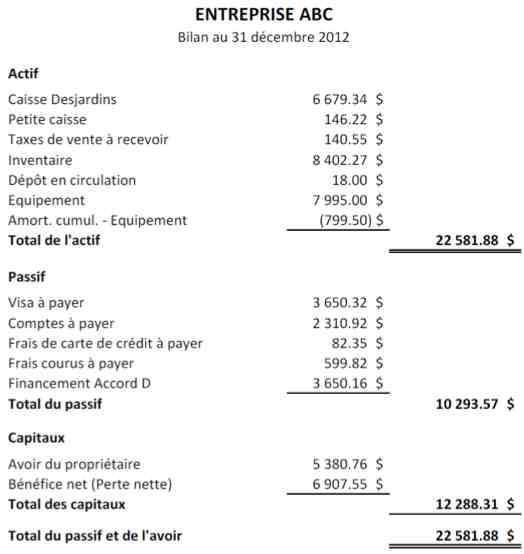

Balance sheet

Noun

A financial report that summarizes a company's assets (what it owns), liabilities (what it owes) and owner or shareholder equity, at a given time.

Example: Finally, an evaluation of the balance sheet and relevant Ratios are also taken into account.

fr: Bilan

Cash flow

noun

The revenue or expense expected to be generated through business activities (sales, manufacturing, etc.) over a period of time.

Example: Essex (2001) Interest rates directly affect a household's cash flow: a change in interest rates alters the immediate burden of mortgages interest payments.

fr: Flux de trésorerie

Chartered Accountant

noun

An accountant who has a certain amount of experience and who has passed certain exams that qualify them to be a member of an institution, such as the Institute of Chartered Accountants in the UK. In the US a similar title is that of Certified Public Accountant (CPA).

Example: She’s been studying to become a chartered accountant for a few years now, but she just couldn’t manage to pass the final exam.

fr: Comptable agréé

Cost of goods sold

Noun

The direct expenses related to producing the goods sold by a business. The formula for calculating this will depend on what is being produced, but as an example this may include the cost of the raw materials (parts) and the amount of employee labor used in production.

Example: In the Sonite market the firm has the lowest 'cost of goods sold and inventory holding costs.

fr: Coût des marchandises vendues

Financial Statements

Noun

Documents that show the financial situation of a company. They include the balance sheet (showing assets, liabilities and shareholders’ equity, see above), the income statement (showing revenues and expenses) and statement of cash flows (showing cash flow fluctuations in a certain accounting period).

Example: The accountants were all busy working on the financial statements as the company was planning to refinance its loans.

fr: États financiers

General ledger

Noun

A complete record of the financial transactions over the life of a company.

Example: A general ledger account (GL account) is a primary component of a general ledger

fr: Grand livre général

Generally accepted accounting principles

Noun

A set of rules and guidelines developed by the accounting industry for companies to follow when reporting financial data. Following these rules is especially critical for all publicly traded companies.

Example: According to Penman, when analyzing the quality of accounting, we seek answers to five questions: Are generally accepted accounting principles (GAAP) deficient?

fr: Principes comptables généralement reconnus

Gross

Adjective

An amount of money before taxes are deducted.

Example: Background The microprocessor industry is one of the most profitable industries (Intel's gross margins can reach 47% on average), virtually dominated by Intel (Kharif, 2002).

fr: Brut

Gross Margin

noun

Gross Margin is a percentage calculated by taking Gross Profit and dividing by Revenue for the same period. It represents the profitability of a company after deducting the Cost of Goods Sold.

Example: Gross profit margin should be stable since change in this ratio can have a significant impact on Net profit for the year and without adequate gross margin, a company will not be able to "pay its operation and other expenses and build for the future".

fr: Marge brute

Insolvency

Noun

A state where an individual or organization can no longer meet financial obligations with lender(s) when their debts come due.

Example: Referred to hereon as IMF Financial crises are defined as follows "Episodes of financial market volatility marked by significant problems of illiquidity and insolvency among financial market participants and or by official intervention to contain such consequences" (Bordo et al 2002: 4) There are three main types of financial crisis according to Bordo et al (2002:4-5), which are banking, currency and twin crises.

fr: insolvabilité

liabilities

Noun

A liability is something a person or company owes, usually a sum of money. Liabilities are settled over time through the transfer of economic benefits including money, goods, or services. Recorded on the right side of the balance sheet, liabilities include loans, accounts payable, mortgages, deferred revenues, bonds, warranties, and accrued expenses.

Example: Jolly SU has no loan history and therefore has no liabilities in the form of loan repayments.

fr: Passif

Liabilities

noun

A company's debts or financial obligations incurred during business operations. Current liabilities (CL) are those debts that are payable within a year, such as a debt to suppliers. Long-term liabilities (LTL) are typically payable over a period of time greater than one year. An example of a long-term liability would be a multi-year mortgage for office space.

Example: For example, taking out liabilities insurance can be very expensive, as can be employing a separate inspector of workmanship or purchasing extra safety equipment.

fr: Passifs

Net income

noun

A company's total earnings, also called net profit. Net income is calculated by subtracting total expenses from total revenues.

Example: It is often justified on the grounds that it separates items of transitory nature from net income and so is reported as part of equity rather than in an income statement.

fr: revenu net

owner's equity

noun

In the most general sense, equity is assets minus liabilities. An owner’s equity is typically explained in terms of the percentage of stock a person has ownership interest in the company. The owners of the stock are known as shareholders.

Example: This means the owner’s equity represents the owner’s net worth of a business. It is the total value of a company’s net assets after all liabilities have been deducted.

fr: Capitaux propres

Provider

noun

a person or thing that provides something.

Example: Mackenzie states that it was mainly 'as a provider of the food-supply that Demeter was addressed.'

fr: Fournisseur

Trial balance

Noun

A business document in which all ledgers are compiled into debit and credit columns in order to ensure a company’s bookkeeping system is mathematically correct.

Example: A trial balance includes a list of all general ledger account totals.

fr: Balance de vérification

Value Added Tax

noun

A tax that consumers pay on most products and services, except most food and drugs. Not all countries have a VAT system. In the US, most states have something similar, called a sales tax.

Example: The bookkeeper had to calculate the Value Added Tax in order to issue the invoice.